Last Friday (December 14), Governor Parnell announced the Administration’s proposed state budget for Fiscal Year 2014. The full speech is available here. Later in the day, the Administration’s Office of Management and Budget released a more detailed summary of the budget and the Executive Summary of the 10-year forecast, required by the Executive Budget Act, that will accompany the budget submission at the start of the legislative session.

Last Friday (December 14), Governor Parnell announced the Administration’s proposed state budget for Fiscal Year 2014. The full speech is available here. Later in the day, the Administration’s Office of Management and Budget released a more detailed summary of the budget and the Executive Summary of the 10-year forecast, required by the Executive Budget Act, that will accompany the budget submission at the start of the legislative session.

The proposed budget is the first in a constitutionally (Art. IX) and statutorily (AS 37.07) outlined process – normally containing three steps – that ultimately will determine the final state budget for the coming fiscal year. The second step is review and revision of the Governor’s proposed budget by the Legislature, ultimately leading to the passage of its own version of the budget. The third step is subsequent review of the legislatively approved budget by the Governor and, if appropriate, vetoes of various appropriations contained in the Legislature’s budget (the so-called, “line item veto” provided by Art. II, Sec. 15 of the Alaska Constitution). In extreme cases, there is some potential for a fourth step should the Legislature decide that the Governor’s vetoes are excessive; the Legislature can (but very seldom does) override any of the vetoes by a two-thirds vote, reinstituting the specific appropriations otherwise stricken by the Governor.

I have written on these pages previously – and extensively – on the need to move Alaska toward a sustainable fiscal policy. (A good description of the sustainable budget model, developed by the University of Alaska’s Institute for Social and Economic Research (ISER), is contained in its “Web Note 13,” available here.) In organizing following the election, the incoming Senate Majority also spoke to the subject, identifying as one of their “Top Three Areas of Focus,” “develop[ing] sustainable capital and operating budgets for current and future generations.”

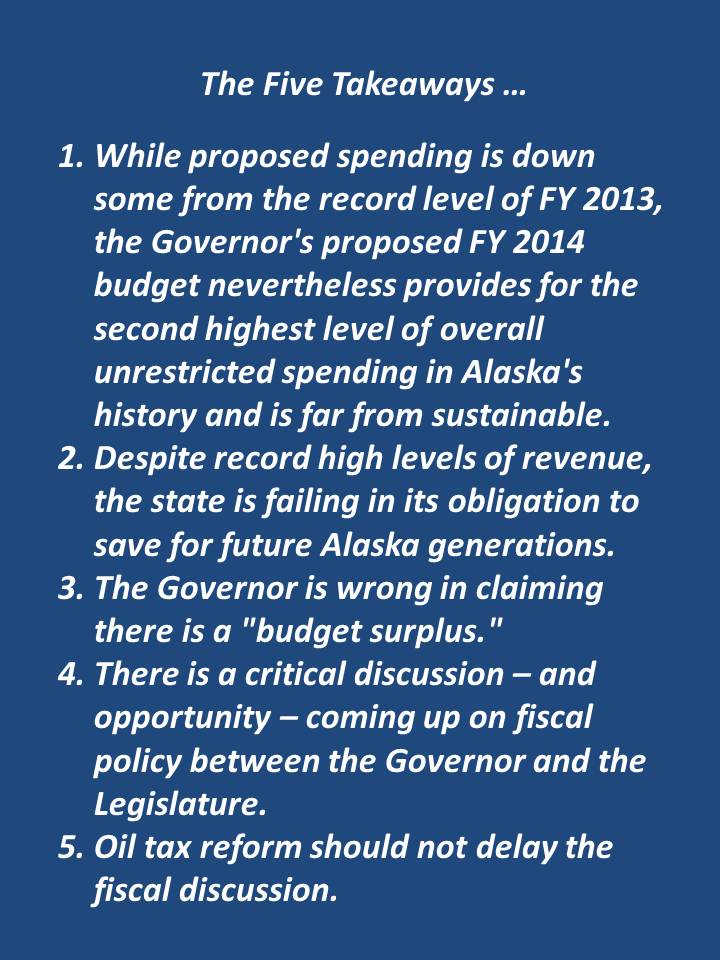

These are my five takeaways from that perspective on the Governor’s proposed budget.

On its face, Governor Parnell’s proposed FY 2014 budget initially contemplates unrestricted general fund spending (combined Operating and Capital) of approximately $ 6.5B, down roughly $ 1.1B from FY 2014 levels. That remains, however, nearly $ 1B (or 16%) over the FY 2013 sustainable level.

Moreover, the spread between the Governor’s proposed budget and the FY 2014 sustainable spending level is likely more. In the course of rolling out the proposed budget, the Governor said that it contemplates a $ 500 million “surplus” (which is wrong, but more about that below), which he said can be used “for legislative budget priorities,” or in other words, added to the spend side of the budget by the legislature. Including that amount, the Governor’s proposed FY 2014 budget is effectively $ 7B, only $ 500 million (7%) short of the FY 2013 record and the second largest state budget – in terms of unrestricted General Fund spending – in Alaska’s history.

In addition, while final calculations are not yet available, the current sustainable budget level is likely lower – and perhaps even significantly lower – than the FY 2013 level of $ 5.6B. A sustainable budget level is calculated based on three components – the balances in the Permanent Fund and the various budget reserves (the Constitutional Budget Reserve, the Statutory Budget Reserve and the unspent balances carried in the various transfer accounts that the Legislature has created over time), and the net present value of the stream of future receipts anticipated from monetization of the state’s resources (i.e., oil & gas royalties and production taxes).

According to the Department of Revenue’s Fall 2012 Revenue Forecast, projected future production – and thus, the projected future stream of revenue – from the state’s resources has dropped materially from those anticipated in the previous, FY 2013 forecasts due to more realistic forecasts. Moreover, as I will discuss further below, rather than saving $750 million in the current fiscal year to the Statutory Budget Reserve as estimated in the FY 2013 budget, the state is now projected actually to lose on net roughly $60 million in the current budget year.

As a result, preliminary FY 2013 calculations suggest that the current sustainable budget level is at or below $ 5B.

Consequently, rather than closing the gap between the state’s spending and sustainable budget levels, the Governor’s proposed FY 2014 budget likely creates the same, and potentially may even widen, as ISER puts it, the level of “fiscal burden” being shifted to future generations of Alaskans. Adding the “surplus” the Governor suggests may be used “for legislative budget priorities” and using as a current proxy $ 5B as the new sustainable budget level, the Governor’s proposed FY 2014 budget likely repeats the same $ 2B overspend as existed in FY 2013 and, if the current sustainable budget level turns out to be lower, potentially exceeds it.

2. Despite record high levels of revenue, the state is failing in its obligation to save for future Alaska generations. Maintaining sustainable budget levels in future years requires that a portion of current revenues be placed into savings, in order to build a sustainable budget “nest egg,” which in turn is used to generate additional, supplemental revenues once oil revenues fall below levels sufficient to sustain current spending levels.

In response to criticisms last year over the approved spending levels, some legislative members effectively argued that the Legislature at least should receive partial credit for providing for some savings.

It is true that the “enacted” budget last year contemplated some transfers to the Statutory Budget Reserve. Based on projected unrestricted General Fund revenues at the time of $ 8.4B, the enacted FY 2013 budget contemplated a contribution of roughly $ 750 million to the Statutory Budget Reserve by the end of the fiscal year. Unfortunately, however, that promise evaporated during the year. Instead of the projected $ 8.4B in unrestricted revenues, the state is now projected to receive roughly only $7.6B during FY 2013, due to lower than anticipated production and prices. Moreover, instead of the projected $ 7.58B in spending approved in the FY 2013 budget, the state now appears on track to spend roughly $ 50 million more.

As a result, rather than adding to overall savings, the state now appears to be on course to end up FY 2013 roughly $60 million in the red, with the difference being made up by a draw from the Statutory Budget Reserve. In short, rather than moderately contributing to Alaska’s fiscal future as some legislators argued they had accomplished during the 2012 legislative session, the reality is that Alaska’s fiscal future has become even more bleak over the course of the past year.

The Governor’s proposed FY 2014 budget makes matters even worse. Instead of starting with projected savings of some level, taking into account the $ 500 million the Governor has suggested be used for “legislative budget priorities,” the Governor’s proposed FY 2014 budget effectively starts with no proposed savings. That means any later adverse budget surprises (which there almost always are), either in terms of lower than anticipated revenue or higher than anticipated savings, will immediately throw the FY 2014 budget also into the red, at the very time future generations are relying on this Governor and Legislature to generate at least $ 2B (and possibly more) in savings from current revenue levels.

In short, rather than moving in a positive direction in terms of building a sustainable fiscal future for Alaska, the FY 2013 results and the proposed FY 2014 budget are moving rapidly in the reverse, creating an even deeper hole in Alaska’s future finances and making Alaska’s fiscal future much, much more difficult. The state simply is not saving enough – indeed, based on current projections and the Governor’s proposed budget, it’s not saving anything at all from General Fund receipts – for future Alaskans.

3. The Governor is wrong in claiming there is a “budget surplus.” Several times during his Friday presentation, Governor Parnell referred to the budget as having a “surplus” that he subsequently described as being available for “legislative budget priorities.” The Governor’s assertion, however, relies entirely on current (and inadequate) state accounting practices. Substantively, the Governor is wrong; the budget does not have a surplus.

When I – and most, if not all of the readers of these pages – make out our personal budgets we always include some amount for retirement. Some of us have our retirement taken out at work, so that we never see it as part of take home check. Some of us don’t – or we don’t have enough taken out – and so, we take the amount out when we receive our checks and put it into savings, or into investments. Either way, accounting for retirement – for a time when our working revenue will not match our expenses – is part of our personal budgets.

We do that because we know there will come a day when we no longer receive a working paycheck, or at least not one that is large enough to cover the style of living that we want to maintain. We anticipate our working income will gradually fall over time – or stop altogether – as we retire, and we will want to have savings – or what some call a “nest egg” – which continues to produce revenue that covers our living expenses once that occurs.

As I have explained previously on these pages, Alaska is in much the same position. Sometime in the future – and perhaps the not too distant future – Alaska will reach a point where its income from oil will no longer cover the reasonable costs of government. Without saving for that day, Alaska will be in the same position as we might be individually in our retirement if we had not put aside savings in the years before. In our personal lives, we would experience a significantly lower standard of living in our retirement, and likely would have to take small jobs to help supplement even that. If Alaska does not save for the day that oil revenues are not sufficient to cover the reasonable costs of government, Alaska – and Alaskans – will either suffer a lower standard of living or the state will have to initiate a governmental form of taking small jobs – in the case of the state, it will have to initiate sales, property and income taxes – in order to continue to pay for the reasonable costs of government.

Some think that the Permanent Fund – which is being built slowly, sort of in the same manner as having a portion of our retirement taken out at work – will provide the necessary cushion to meet Alaska’s revenue requirements when oil no longer does. It will not. At its current size, the Permanent Fund (and other current savings accounts) are capable of delivering steady revenue only in the range of $ 2.5 – 3B per year. As we have seen above, however, current state government budgets are consuming in the range of $ 6 – 7B per year. As a result, Alaska needs to be supplementing the “retirement” savings being put into the Permanent Fund in the same way as we do as individuals. Alaska needs to be setting aside additional money out of current earnings – its paycheck – in order to prepare for the day when those paychecks are no longer adequate to meet ongoing expenses.

That step – putting additional money aside for future generations – should be as much a budget priority as anything else, but it is not currently reflected or accounted for anywhere in the current budgeting process. If it were – as it should be – there would be an account set up for building the “nest egg.” The additional amount to saved out of current revenues – which ISER estimates currently is around $ 2B per year – would more than offset the so-called “budget surplus” the Governor claimed in his Friday presentation.

The fact that the state has not yet set up the formal account does not mean that there is a “surplus.” It may seem like there is, just as it might seem that our own budgets have a “surplus” if we don’t include the annual amounts required to be contributed to our own individual retirement savings. There is no actual “surplus,” however; we simply have failed properly to account for all of our expenses.

4. There is a critical discussion – and opportunity – coming up on fiscal policy between the Governor and the Legislature. During his Friday presentation, the Governor said that he wants to have a discussion with the Legislature about agreeing on a spending limit. As mentioned above, he said that he is prepared to increase the initial levels proposed in his budget to allocate to “legislative priorities” the $ 500 million in “surplus” he claims the budget provides.

Importantly, however, he also said he is prepared to work with the Legislature, if it wants, to reduce the budget “and put more in savings than the $508 million that is currently calculated.” That is the direction in which the state desperately needs to move if it is to prepare for its future and keep faith with future Alaskans. As a result, the coming discussion between the Governor and Legislature will be one of the most critical on fiscal policy in the state’s history.

As I have explained elsewhere on these pages and in other publications, there is very little time remaining if the state is successfully to implement a sustainable budget model and, by doing so, keep faith with future Alaskans. Developing a sustainable budget depends on putting money into the “nest egg” now, while oil revenues are higher than current, reasonable spending levels. Even a short delay in doing so – by failing to save in years where oil revenues remain high – results in a lower nest egg, a lower payout in future years and, because there is less in the nest egg, correspondingly requires a higher contribution from current revenues, once they begin, in order to build up the nest egg even moderately going forward. Every year that there are insufficient savings, current Alaskans are hurting themselves (along with future Alaskans) by creating a need to save even more – and as a consequence, have less available to spend – once they recognize the need to start accounting for supplemental future revenues.

According to every one of the scenarios plotted in the ten-year forecasts accompanying the Governor’s FY 2014 proposed budget, the cross-over point – the point at which the state will need to start using savings to supplement oil revenues in order to maintain spending – will come at some point in the next ten years.  Some scenarios predict an earlier point – for example, one scenario assumes that Alaska North Slope oil drops and then stabilizes at $90/bbl (see chart). Under that scenario, Alaska already has hit the cross-over point, with deficits growing to more than $ 3B/year by FY 2023, the end of the period. The cross-over point under other scenarios doesn’t come until later in the period – for example, another scenario assumes that the budget remains capped at $ 6.8B during the entire ten-year period, with oil prices continuing to fluctuate but never going below $110/bbl and reaching over $125/bbl by the end of the period. Even under that scenario, however, Alaska hits the cross-over point by FY 2020, and is running deficits of more than $600 million by the end of the ten-year period.

Some scenarios predict an earlier point – for example, one scenario assumes that Alaska North Slope oil drops and then stabilizes at $90/bbl (see chart). Under that scenario, Alaska already has hit the cross-over point, with deficits growing to more than $ 3B/year by FY 2023, the end of the period. The cross-over point under other scenarios doesn’t come until later in the period – for example, another scenario assumes that the budget remains capped at $ 6.8B during the entire ten-year period, with oil prices continuing to fluctuate but never going below $110/bbl and reaching over $125/bbl by the end of the period. Even under that scenario, however, Alaska hits the cross-over point by FY 2020, and is running deficits of more than $600 million by the end of the ten-year period.

As I have explained elsewhere on these pages, the “future is now” in terms of adopting a sustainable budget. Looking at the ten-year forecasts, if the Governor and Legislature fail to initiate a savings and sustainable budget plan this year, the potential benefits will be significantly diminished, and the hill left for future generations to climb will be substantial. As a result, the discussions this year between the Governor and Legislature on fiscal policy, at least from the perspective of future generations of Alaskans, are critical. They should be approached carefully, seriously and with a great deal of thought about the consequences of the decisions that are made.

5. Oil tax reform should not delay the fiscal discussion. Some are likely to argue in the coming days that fiscal reform should wait on the completion of oil tax reform – and indeed, even longer, on seeing the consequences of oil tax reform. Those who make the argument likely will suggest that oil tax reform will result in increased future production, an improved financial picture and as a consequence, less of a need for building a sustainable budget. Based on that assumption, some are likely to argue that the state can maintain its current spending levels in the meantime.

Remaining Life at Various Investment Levels

Click to enlarge

That approach is an unacceptable diversion. Done correctly, oil tax reform will likely result in an improved future production profile, but while improved, the trend line – at least for production from state lands, which is the source of almost all of the state’s revenue – is still likely to remain a long term decline. (See the graphic to the left for a previous estimate of how oil tax reform is likely to improve production — and revenues).

Oil is a depleting resource and the facts are, even with oil tax reform, at some point in the foreseeable future oil revenues will be insufficient to meet the state’s revenue requirements. As I discuss above, the generation of Alaskans living here then will be faced with a significantly reduced standard of living, either as a result of much lower state spending, the requirement that they pay sales, property and income taxes to support state spending, or, most likely, both.

As others have often noted, the Constitution provides at Art. VIII, Sec. 2 “that the legislature shall provide for the utilization, development, and conservation of all natural resources belonging to the State … for the maximum benefit of its people.” That provision isn’t limited only to those who are citizens at the time the resource is developed; it applies to all of the state’s “people,” without limitation on generation. Without developing a sustainable budget, current Alaskans inevitably are going to consume most, if not all, of the benefit of the state’s oil, without sharing a portion of the significant benefit also with future generations. In order to preserve an appropriate portion of the benefit for future generations, the Governor and Legislature need to start setting aside a portion of the current financial benefit now.

Such an approach will not unduly limit future spending if oil tax reform results in the development of additional production. Assuming oil reform is passed and results in additional future development, the sustainable budget model automatically will adjust. The component linked to the net present value of the stream of future oil & gas royalties and production taxes will increase, reducing the portion of the nest egg that needs to be accumulated from current savings. Implementation of the policy simply will ensure that, regardless of the outcome, future generations of Alaskans are treated equitably with the current generation.

Pingback: “Five takeaways from the Governor’s proposed budget …”: The Radio Interview | Thoughts on Alaska Oil & Gas

Pingback: Alaska Fiscal Policy| Another reason to be concerned about state spending, NOW … | Thoughts on Alaska Oil & Gas

Pingback: Alaska Fiscal Policy| On the Dan Fagan Show Wednesday (Jan. 2) | Thoughts on Alaska Oil & Gas

Pingback: “Five takeaways from the Governor’s proposed budget …”: The Radio Interview | Thoughts on Alaska Oil & Gas

Pingback: Alaska Oil Policy| The Need for a Sustainable Budget | Thoughts on Alaska Oil & Gas

Pingback: Alaska Oil Policy| The Governor commits an unforced error … | Thoughts on Alaska Oil & Gas

Pingback: Alaska Fiscal Policy| Casey Reynolds nails it: The Governor isn’t a fiscal conservative at all … | Thoughts on Alaska Oil & Gas