In discussing the purpose behind the creation of the Permanent Fund and later the Permanent Fund Dividend former Governor Jay Hammond outlined a very simple, two part plan:

In discussing the purpose behind the creation of the Permanent Fund and later the Permanent Fund Dividend former Governor Jay Hammond outlined a very simple, two part plan:

The first related to the creation of the Permanent Fund itself:

I wanted to transform oil wells pumping oil for a finite period into money wells pumping money for infinity. …

The second focused on what to do with the earnings, once the “money wells” were pumping:

Each year one-half of the account’s earnings would be dispersed among Alaska residents …. The other half of the earnings could be used for essential government services.” Diapering the Devil, https://goo.gl/FFTi9M at 15, 19.

Through Constitutional amendment (Art. 9, Sec. 15, https://goo.gl/rSxZ9n) and statute (AS37.13.145, https://goo.gl/rfScqh), the state has implemented the first and the first half of the second (“one-half of the account’s earnings would be dispersed among Alaska residents”) parts of the plan.

The state never, however, has implemented the second half of the second part of the plan (“The other half of the earnings could be used for essential government service.”). Instead, the state repeatedly has drawn on savings when it has needed supplemental sources of money to fund essential government services rather than turning to the “other half” of earnings.

Now that some have suggested the use of savings should be reduced — and replaced by taking money from the state’s private economy through PFD cuts and/or taxes — we have examined what it would take to implement the final step of Governor Hammond’s 50/50 plan.

The potential benefit is significant. The portion of the earnings stream annually being “dispersed among Alaska residents” is roughly $1.4 billion. Assuming that represents “one-half of the account’s earnings,” which it does when averaged over time, that means there should be roughly an additional $1.4 billion in annual earnings currently that “could be used for essential government services” before drawing money from the state’s private economy.

In fact, that additional earnings stream is there and, as Governor Hammond envisioned, it could be tapped. But instead of doing so the Governor and legislature inexplicably are looking past it and talking about cutting the PFD or implementing new taxes instead.

They shouldn’t.

The “Other” 50%

The “other” 50% is in two pots.

The first is an accumulation of the “other” 50% received, but left unused, in prior years , that is now sitting as a result untapped in the earning reserves account.

Under AS 37.13.145, all of the statutory earnings produced each year from the Permanent Fund first go to the earnings reserve account. From there, the “one-half … [to] be dispersed among Alaska’s residents” is sent to the dividend fund. The remaining “one-half” remains in the earnings reserve.

Of that remaining one-half, a portion historically has been sent back into the Permanent Fund corpus for inflation proofing. We will discuss that further in a moment.

The portion that remains after that is the accumulated, residual “other half” envisioned by Governor Hammond to be available for “essential government services.” As the accumulated residual it is, in essence, another savings account available for use to help fund “essential government services,” when needed.

The size of that additional, previously untapped savings account is substantial.

According to the legislature’s Legislative Finance Division, the estimated balance in this additional savings account as of the end of the current fiscal year will be somewhere in the neighborhood of $9 billion, https://goo.gl/u1No6p at 3, more than twice the size of the CBR.

Under Governor Hammond’s 50/50 approach, that savings is intended to help fund “essential government services.” It should be used long before making cuts in the state’s private economy.

The Remaining “Other” 50%

The second pot containing the “other” 50% is the portion of the ongoing annual earnings stream that remains after paying dividends.

In another piece recently we used the Permanent Fund Corporation’s “Fund Financial History and Projections” to explain our point (see, Bill Walker’s “Pants on Fire” claim about the PFD, https://goo.gl/kPL363). We do the same here.

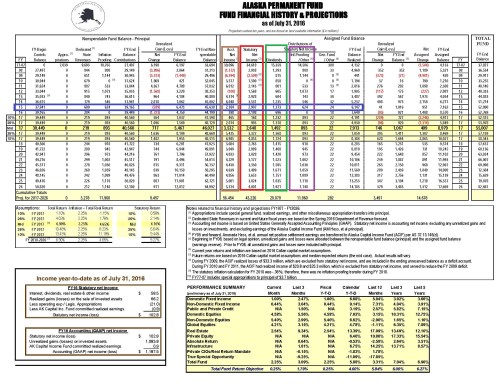

Right click on image and open in new tab to enlarge

The column outlined in red above (“Statutory Net Income”) is the annual earnings stream used to calculate the PFD. The annual amount taken for the PFD is outlined in green (“Dividends”). Because the PFD is calculated based on a five year rolling average the amount taken annually for dividends does not equal 50% of the earnings stream occurring in any given year, but it does equal 50% of the earnings stream over time.

As is clear from the chart, there is a significant amount of earnings remaining each year after deducting the PFD. For example, in FY 2015 (outlined in blue), the difference between earnings and dividends was $1.534 billion ($2.907 B earnings – $1.373 B dividends). That is the annual replenishment of the “other” 50% which Governor Hammond contemplated could be used to help fund “essential government services” when needed, but never has been.

Historically, a significant portion of that “other” earnings stream has been put back into the Permanent Fund as “inflation proofing” (outlined in purple on the chart). But, to be honest, that is a historical artifact and no longer necessary.

The reason is because as the Permanent Fund Corporation’s management of the fund has matured over the years it has adopted investment practices that essentially inflation proof the fund in a different way.

Again going to the chart, we have outlined an additional column in brown (“Acct. Net Income”). That represents all income accrued during any given year on investments, including gains in the value of stocks and other invested assets that have not yet been “realized” (i.e., converted to cash). The portion converted to cash is treated as “Statutory Net Income.”

Because only cash income (the red column) is used in the calculation of the dividend, the additional, non-cash income automatically goes back into the fund each year. As the Corporation’s investment approach has matured over time, that additional amount essentially has come to inflation proof the fund on its own. Looking over the next several years, for example, the Corporation projects the Fund annually will earn an overall return of about 6.7% (“Acct. Net Income”), but only pay out in dividends and other potential cash draws (“Statutory Net Income”) about 5%.

The difference — 1.7% — will be retained in the Fund and because it already is slightly more than the average 1.5% inflation rate projected by the Corporation over the same period, will not only cover inflation but also provide a more than adequate cushion against unanticipated changes.

Given that, the additional contribution toward “inflation proofing” made by sending funds from the annual cash earnings back into the Permanent Fund corpus is unnecessary and, results, essentially in double counting for inflation. Taking into account both the implicit inflation adjustment reflected in the difference between “Acct. Net Income” and “Statutory Net Income,” and the explicit adjustment contemplated by the statutory “inflation proofing” contribution made from the earnings reserve, the current methodology is projected to set aside more, and in some years much more, than 3% for inflation over the next ten years. Yet, the actual inflation rate projected over the same is only around 1.5% on average.

Such double counting for inflation is wholly unnecessary.

As a result, that portion of the “other” 50% currently being sent back into the Permanent Fund corpus for “inflation proofing” (projected to average around $1 billion annually over the next several years) instead should be retained in the earnings reserve and used, as Governor Hammond intended, to help pay for “essential government services,” when needed.

The significance of using the “other” 50%

As Alaska has progressed through its current fiscal situation, Governor Walker and others increasingly have talked about finding “new” revenues to fund Alaska government.

By that they generally have meant taking existing revenues out of the state’s private economy through either PFD cuts, new taxes or a combination of both and transferring the balance to the government economy as “new” (to it) revenues.

The problem with that approach is, depending on the way in which the money is taken from the private economy and the things on which it is spent by government, it can have a a negative effect on the overall Alaska economy.

Earlier this year, the University of Alaska-Anchorage Institute of Social and Economic Research — the state’s best economic think tank — analyzed the overall economic effects of various options. Short-Run Economic Impacts of Alaska Fiscal Options, https://goo.gl/ZxR1Hw (March 2016).

Applying the factors in that analysis we later calculated the various economic effects of taking money from the private sector and respending it in the government sector. While some combinations had a positive economic effect on the overall economy, more had a negative effect, and all had at least some offsetting effects. https://goo.gl/p8J7He

The benefit of Governor Hammond’s approach is that it does not take money out of the private economy in order to provide “new revenues” to the government economy. While eliminating the double contribution for inflation does reduce somewhat the growth rate of the Permanent Fund corpus, the step nevertheless retains the approach to building the corpus of the Permanent Fund always envisioned by Governor Hammond.

And in doing so frees up what is projected to be roughly $1.4 – 1.5 billion annually in what are truly “new” revenues — in the sense that they are not being repurposed out of the private economy — over the next five years.

The economic mechanisms Governor Hammond envisioned at the time the Permanent Fund and Permanent Fund Dividend were established remain as relevant and helpful to Alaska today as at the time they were created.

In the next legislative session Alaska should finally implement the remaining portions of Governor Hammond’s 50/50 plan. Doing so will be a major step forward in finding a fiscal solution that benefits all Alaskans, not just the select few tied to the government economy.

You must be logged in to post a comment.