As thoughts begin to turn to the now-certain referendum on SB21 it is important to understand that there is one scenario under which the Governor himself could end up significantly undermining a key argument for maintaining the statute.

As thoughts begin to turn to the now-certain referendum on SB21 it is important to understand that there is one scenario under which the Governor himself could end up significantly undermining a key argument for maintaining the statute.

The scenario relates to the interplay between SB 21 and the budget. Interestingly, the Governor likely has complete control over whether the adverse scenario develops. Unfortunately, current indications are that he is headed down the wrong path.

The Reasons Supporting SB 21

On the surface, there are two major arguments supporting SB 21. The first is that it produces greater long term value to Alaskans from oil than ACES, the previous tax policy to which the law will return if SB 21 is repealed and as a result, against which SB21 should be compared. The second is that, by spurring greater investment and oil field activity, SB21 will improve the long term outlook for jobs both directly in the oilpatch, and indirectly in the service and other sectors of the state.

The second argument is difficult to use as a stand alone argument, however. Because the state has no income, sales or property taxes, there is little direct return to the state from increasing the number of jobs. If jobs increase, but the total long term value to Alaskans from oil declines, the measure begins to look like it is a targeted subsidy, trading off reduced state wealth for jobs for a select few, only some of which will go to Alaskans and even then, only some of whom will remain in Alaska, and thus continue to contribute to the Alaska economy, for the long term.

As a result, at the end of the day the argument for SB 21 really comes down to the claim of increased wealth. Jobs can act as a tie-breaker — that is if both SB 21 and ACES produce near the same level of value, the fact that SB 21 results in an increased number of jobs for Alaskans can decide the argument in its favor. But jobs alone likely cannot carry the day if the value argument fails.

To this point SB 21 has carried the value argument. As I have noted elsewhere on these and other pages, in the latter stages of the consideration of SB 21 before House Finance, EconOne, the oil economists retained by the Administration, provided a series of comparisons (at p. 13-19) of future revenue streams under ACES and SB 21. These analyses demonstrate that SB 21 will produce a greater net present value for the state than ACES at all long term price levels between $90 and $140/bbl ($2012), assuming that the revision results in at least a slight bump in long term investment, and thus, production levels over those otherwise anticipated under ACES. I believe that is a fair assumption, backed up well during the legislature’s deliberations.

As is clear to those who have studied those numbers, however, that outcome is highly dependent on SB 21 continuing to generate the anticipated investment bump — and thus, production bump — over a sustained period. As the Administration’s own Fiscal Note on SB 21 succinctly demonstrates, in the near term state revenues are lower under SB 21 than ACES . The EconOne analysis demonstrates that the deficiency ultimately is overcome as production rises to levels which, even at the lower tax rate, result in higher overall state revenues.

But that effect takes some time. The EconOne comparison, for example, calculates its comparisons over a 30-year period.

The Impact of the Budget

That is where the interplay with the budget comes in. As I have explained in a previous piece for Alaska Business Monthly (“Alaska Oil Policy| Understanding Investment“), industry investment depends not only on current taxes, but also on projections of future taxes anticipated to apply over the entire revenue stream of a project. Investors will not make the required upfront investments necessary to increase production if they anticipate taxes will increase significantly over the course of the resulting revenue stream, to the point that the project no longer produces as competitive a return as alternative investment opportunities.

Unfortunately, as I also have explained on these pages and others, current projections about future Alaska tax rates are murky, at best, because of the fiscal policy the state is following. As the University of Alaska – Anchorage’s Institute of Social and Economic Research (ISER) has made clear, at current spending levels “[r]easonable assumptions about potential new revenue sources suggest we do not have enough cash in reserves to avoid a severe fiscal crunch soon after 2023, and with that fiscal crisis will come an economic crash.”

That forecast was made based on revenue levels which assumed a continuation of ACES. As I have explained in a recent Alaska Business Monthly piece (“Alaska Oil Policy| Missing the Point“), however, the result remains true also under the revenue levels forecasted for SB 21 by EconOne.

Oil and other resource companies are highly sophisticated economic analysts. They know Alaska’s history and its dependence on oil revenues to fund state government, and will reasonably assume that as Alaska approaches the “fiscal crisis” and “economic crash” forecast at current spending levels by ISER , the state is likely to respond once again, at least in part, by raising oil taxes.

Based on that, investors will start significantly to slow down the rate and level of investment as the related economics begin to depend on revenue streams which overlap with the period during which taxes are likely to be raised.

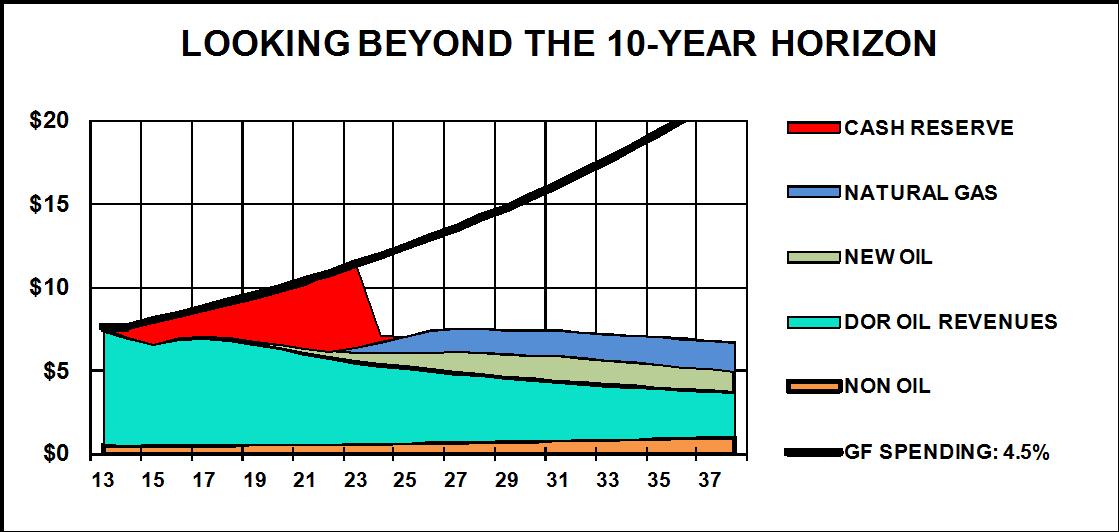

I describe a typical investment revenue stream in “Understanding Investment.” Overlaying that on the graph at the left, which shows the time remaining until the “economic crash” forecast by ISER is likely to occur at current spending levels, reveals that the fiscal policy-induced slowdown in investment likely is not far off, and will occur well before the point at which higher production rates from SB 21 are projected to offset the revenue losses incurred in the earlier years.

I describe a typical investment revenue stream in “Understanding Investment.” Overlaying that on the graph at the left, which shows the time remaining until the “economic crash” forecast by ISER is likely to occur at current spending levels, reveals that the fiscal policy-induced slowdown in investment likely is not far off, and will occur well before the point at which higher production rates from SB 21 are projected to offset the revenue losses incurred in the earlier years.

As a consequence, before SB 21 has a chance to rebuild production to volumes which offset the lower tax rates, at current spending levels a fiscal policy-induced slowdown in investment will occur which will negate the likelihood of achieving the anticipated production gains. Put another way, because of the failure to curb state spending, the production renaissance anticipated to result from SB 21 will be truncated before it begins to pay off.

If that occurs, SB 21 will end up end up producing a lower long term value to Alaskans than the continuation of ACES.

The Governor’s Opportunity

The future does not have to be this way. As the ISER analysis makes clear, the coming state fiscal crisis can be avoided by reducing spending. As ISER puts it, “[w]hat can the state do to avoid a major fiscal and economic crisis? The answer is to save more and restrict the rate of spending growth. All revenues above the sustainable spending level of $5.5 billion … [sh]ould be channeled into savings.”

If the fiscal crisis is avoided, so is the related fiscal policy-induced slowdown in industry investment and, as forecast by EconOne, the production growth anticipated by SB 21 likely will continue to the point that it exceeds the net present value otherwise anticipated under ACES.

But the ISER analysis makes clear that the time to avoid the fiscal crisis is limited. If the significant spending reductions required to achieve sustainable spending levels are not initiated in the very near term, the window of opportunity to avoid the “fiscal crisis” and “economic crash” will be lost and the dominos will start to fall.

That is where the Governor comes in. In Alaska, more so than in almost any other state, the Governor controls the size of the state budget. Under the Constitution, he proposes the budget at the outset of a legislative session and has line item veto power over the outcome at the end.

So, for example, consistent with ISER’s advice he can propose a budget which reflects spending at $5.5 billion at the front end of the next legislative session, and then veto it to the same level at the back end if the legislature in the meantime passes something greater. The only limit on his power to constrain spending is if the legislature overrides the line item vetoes by three-fourths vote, something which is highly unlikely.

Unfortunately, however, the Governor currently is headed down a much, much different path. Toward the end of the last legislative session the Governor announced that he was satisfied with a budget level of $6.8 billion, nearly 25 percent higher than outlined in the ISER analysis before the start of the session. Much more ominously, at the same he announced that he intends to continue spending at the same, highly elevated level (with the possibility of even higher levels to support “statewide legacy projects”) for the next five years.

Admittedly, those spending levels are somewhat lower than assumed in the ISER analysis made the preceding January. But with the passage of SB 21, the anticipated revenue levels also are lower. Taking both into account, the deficit levels (the difference between spending and revenues), which ultimately drive the timing of the fiscal crisis, are roughly the same as previously used by ISER, meaning that the timing of the resulting “fiscal crash” also remains roughly the same.

As a result, rather than supporting the achievement of SB 21’s objectives, due to the excessive spending levels he previously has approved and continues to advocate, the Governor currently is headed down a path of undermining them.

The Effect on the Referendum

The potential effect on the referendum of the Governor’s current course is clear. The primary argument supporting SB 21 is its potential to create additional wealth for Alaskans. The Governor, however, will severely, if not completely, undermine that argument if at the end of the next legislative session the state remains on a collision course with the “fiscal crisis” and “economic collapse” forecast by ISER.

The Governor may continue to mouth the words — more production and more value for Alaskans — but the underlying support for the argument will ring hollow. Looking down the barrel of a state fiscal gap of unprecedented proportions, because the current level of spending is of unprecedented proportions, current and potential investors will likely defer making significant long-term investment commitments. Without those investments, the production gains anticipated to result from SB 21 will fail to materialize.

If the long term investment on which SB 21 depends is not going to occur, then the better value proposition for Alaskans may be remaining with ACES. While continuing with ACES will destroy long term investment in Alaska, the Governor will be on track to do the same by continuing with his current fiscal policy. With both policies leading to a demise in long term investment, the debate necessarily will shift to which course produces more value to the state in the short term. The answer to that is ACES.

The coming referendum should be about what is right for Alaska, not only for this generation but those that follow. Between the two choices SB 21 is the correct answer, assuming that the long term investment outlook for Alaska remains strong.

To make that case, however, the Governor has to adopt also a forward looking fiscal policy. This Administration has yet to do that and, based on his statements earlier this year, remains clearly committed to the wrong path. Continuing down that path will doom the arguments supporting SB21.

One day last week on his morning radio show Casey Reynolds spent a significant amount of time talking about the the coming referendum on SB 21. (Listen to the podcast of the show here). Focusing on what I agree is the larger issue, Reynolds tied the SB 21 vote to fiscal reform and suggested that fiscal conservatives ultimately may condition their support for SB21 on seeing significant spending reductions and a commitment to a long term, sustainable fiscal plan this coming legislative session.

He may very well be right.

The effort to increase long-term investment in this state is a two-part battle. The first part, modifying the oil tax, is done. But the Governor can’t declare victory at half time and fail to take the field for the second half. The second half — bringing fiscal policy into alignment with long-term investment — is about to begin. The Governor — or someone — needs to suit up and take the field.

You must be logged in to post a comment.