The short answer is pretty damned deep, a lot more than they are proposing to cut government spending.

The short answer is pretty damned deep, a lot more than they are proposing to cut government spending.

One of the things I spent time on while preparing for my presentation last week to the Alaska Republican Assembly (“A Way Forward on the #AKbudget“) was understanding the effect on the PFD of the Governor’s and GCI’s proposed fiscal plans.

It’s not necessarily an easy thing to do. Both the Governor’s and GCI’s fiscal plans propose to change Alaska’s fiscal structure significantly, with the effect that it is challenging to trace the sources and uses of funds in place under the state’s current fiscal approach to how and where they are used under the proposed plans. But it is possible, with some patience.

In analyzing the effect on the PFD of the proposed plans, the key piece of data comes from the Permanent Fund Corporation (PFC), which periodically estimates the total amount of money which likely will be paid as dividends over the following 10 years under current law. The most recent forecast was made as of November 30 this year, and is posted here.

By completely reformulating the way in which the PFD is calculated, both the Governor’s and GCI’s fiscal plans significantly reduce the amounts proposed to be paid. By one means or another, both plans then take the remainder of the revenue stream that otherwise would go to support the dividend and use it, instead, to support government spending.

In the spreadsheets accompanying both plans it is possible to identify the revised level of dividends which would remain under each, and by subtraction from the PFC’s estimates, the amount which each plan proposes to cut from the PFD and convert to general government revenue. The spreadsheets supporting the Governor’s plan are posted here; those supporting GCI’s plan are posted here.

One additional adjustment is necessary to analyze the effect of the Governor’s proposed plan. In addition to cutting the level of the PFD, the Governor’s plan also proposes to establish and increase various taxes. At a macroeconomic level the taxes can be viewed simply as yet another way for government to claw back to itself some of the money that otherwise currently is being injected into the private economy through the PFD.

As a result, in estimating the overall effect on the PFD of the Governor’s approach my analysis also reduces the level of the PFD by the increased amount of money being taken out of the state’s private economy through new and increased taxes. This approach may slightly overstate the adverse effect of this part of the Governor’s proposal because some of the proposed taxes will be paid by those from Outside, and thus, not go to reduce the amount of money otherwise being injected into the local economy through the PFD. But most estimates of that effect are only in the range of 15% (of the tax revenue to be paid from those Outside) and, thus, don’t significantly affect the net numbers.

Charts of the effect of each approach follow. The analysis of the Governor’s approach is first:

As indicated, the blue line at the top of the bars (and the total number for FY 2026) represents the total amount (in $Billion) paid in the past and projected by the PFC to be paid out in the future as PFD’s under the current statutory dividend formula. From 2018 forward, the portion underneath the line — the amount otherwise to be projected to be paid as dividends –is divided into the amount which would continue to be paid as dividends under the Governor’s plan and the amount that would either be retained by the state for government spending in the first instance or clawed back through taxes.

Interestingly for all of the attention the Governor’s tax proposals have received, the chart hi-lites that, between the two, the vast bulk of the “new revenues” his proposal raises are from diverting to government a portion of what otherwise would be paid out as PFD’s under the current statutory formula. The ratio of money raised as a result of cutting the PFD to that raised by taxes is nearly 2:1 from the start, and approaches 2.5:1 by FY 2026.

More interestingly, the negative number in the “Gov(PFD)” line for FY 2026 indicates that, by then, the amount taken in taxes will exceed the (small) remaining amounts paid from the PFD, for a net negative effect on the private economy. That is, in 10 years under the Governor’s plan the PFD program will go, on net, from a wealth generating program for the state’s citizens to, on net, a wealth generating program for state government.

Before taxes, the Governor’s approach cuts the PFD right off the bat in FY 2018 by a staggering 61%, increasing to 76% by FY 2026. Including the tax “claw back,” the Governor’s plan effectively converts 90% of the PFD to government spending in FY 2018, trending up to 106% (as noted above, taking back more in taxes than being paid out in the form of a PFD) by FY 2026.

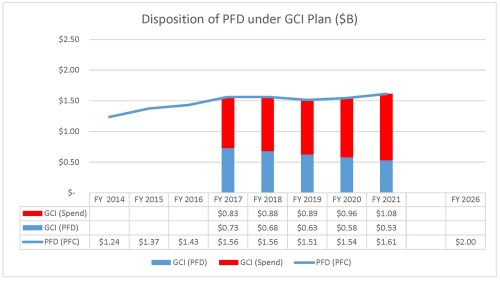

The analysis of the GCI approach is here:

As with the previous analysis, the blue line at the top of the bars represents the total amount (in $Billion) paid in the past and projected by the PFC to be paid in the future under the current statutory dividend formula. From 2017 forward, the portion underneath the line — the amount otherwise to be projected to be spent on dividends — is divided into the amount which would continue to be paid as dividends under GCI’s plan and the amount that would be retained by the state for government spending.

To this point the GCI plan has not included taxes and so, no additional adjustment is made for that. It is interesting, however, that because of the differences in how each calculates the amount available for distribution, from 2019 forward the GCI plan takes more PFD revenue for government, before taxes, than does even the Governor’s plan. From cutting dividends by more than 56% in FY 2018 (compared to the Governor’s 61%), the GCI plan rapidly escalates, cutting dividends by more than 67% by FY 2021 (compared to the Governor’s pre-tax 60%).

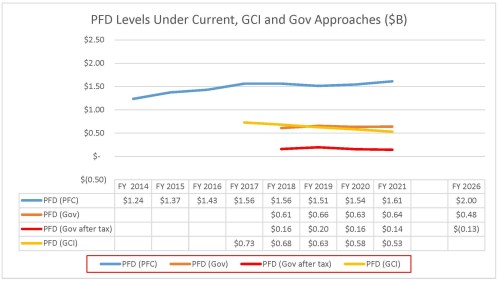

An analysis of the amount of PFD distributions under the current approach compared with the amounts remaining under the GCI approach and the Governor’s approach (before and after accounting for taxes) follows:

As I explained in my presentation last week (at p. 14-15), I have deep concerns about both the Governor’s and GCI’s proposals to cut the PFD.

And it isn’t just me. As Scott Goldsmith previously observed in a 2010 paper, cutting the PFD in order to increase the amount of money spent by government could have adverse consequences for the overall Alaska economy:

Whatever the pattern of purchases and consumption over time, most of the cash from dividends will ultimately find its way into the Alaska economy to increase employment, population, and income. A rough estimate of the total (direct and indirect) macroeconomic effects of this increase in purchasing power is 10 thousand additional jobs, 15 to 20 thousand additional residents (drawn to the state because of the jobs), and $1.5 billion in additional personal income. …

[If the dividend instead had been diverted to state government,] the most likely alternative use of the PFD would probably have been to increase capital spending by state government. … If the money appropriated for dividends had instead gone to capital projects, economic activity would have been generated, just as has been the case with the dividend; but both the macro- and microeconomic effects would have been different. Capital spending would have generated less employment and increased income inequality.

And as former Senate President Clem Tillion observed last week in a column in the Alaska Dispatch News (“The boom may be over, but stealing from the future won’t serve Alaskans“):

I, for one, would … never reduce the amount of the Permanent Fund dividend, for to even consider capping [the PFD] is in itself a major tax, and a tax paid only by Alaskans.

Given the size of the PFD cut under both the Governor’s and GCI approaches, the size of the PFD “tax”, to borrow Tillion’s term — and consequently, the adverse economic effect describe by Goldsmith — proposed by either is substantial.

Hopefully, the Legislature will think twice — and maybe even four, five or twenty times — before adopting either. Cutting the PFD immediately by more than half, and increasing that to nearly 70% (GCI) or effectively eliminating it entirely by FY 2026 (as occurs under the Governor’s approach, accounting for taxes) will have a major, major impact on Alaska’s private economy.

Government may avoid a “recession,” but Alaskans as a whole? Not so much.

Pingback: The Morning Headlamp—Gov. Walker’s self-evaluation - AK HEADLAMP

Pingback: Cuts to PFD much, much deeper than cuts to spending under Governor’s, GCI plans … | Thoughts on Alaska Oil & Gas