Yesterday, EconOne, the Administration’s consultants on oil tax reform, presented an extended analysis to the House Finance Committee of anticipated state revenue levels under various oil tax scenarios. See Modified Slides EconOne 4-10-2013 (Apr. 10, 2013). The analysis projects, under various assumptions, anticipated state revenues from SB 21 compared with ACES over the next 30 years.

The analysis is intended to — and does somewhat — bolster the case for SB 21, the Governor’s proposed oil tax reform. The analysis shows that, with a production response, SB 21 (at either a 33% or 35% base rate) will result in more revenues to the state over a 30 year period than those anticipated to result from ACES. (The analysis also shows that, over the same period, there is not much of a difference between a 33% and 35% base rate.)

In the course of proving that point, however, the analysis provides another data point which severely undercuts the Governor’s recently announced 5-year Fiscal Plan. In essence, the analysis admits what the Governor himself won’t — that Alaska’s current state spending levels, under any set of oil tax assumptions, are an economic disaster in the making.

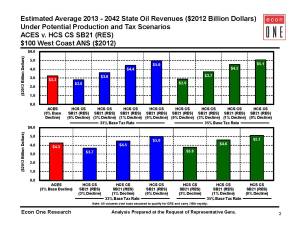

The EconOne analysis is done at several assumed oil price levels. While the slide deck does not break down the calculations by year, at an average price of $100/bbl (in $2012) the analysis concludes that over the next 30 years state oil revenues are likely to average somewhere between $3.3 – 4.3 billion/year under ACES (assuming a 6 or 3% production decline rate), and somewhere between $3.8 – $5.1 billion under SB 21 (assuming a 3, 1 or 0% production decline rate).

Unless the EconOne forecast predicts a substantial change in real oil prices over the 30 year period (unlikely), the numbers shown for the 0% decline rate should roughly approximate what Alaska can anticipate as revenue both in the early as well as during the later years of the 30 year period (at $2012). Under the best of the assumptions included in the analysis at $100/bbl, the resulting annual revenue level under that scenario is $5.1 billion/year. For budgeting purposes, add to that the roughly $500 million that Alaska receives annually as unrestricted general fund revenue from non-oil sources.

As he recently explained in an extended interview, however, the Governor proposes to maintain state spending over the next five years at $6.8 billion, not counting additional amounts spent on “state-wide legacy projects.” As a consequence, even EconOne’s best case scenario at $100/bbl suggests that the Governor likely is putting Alaska on course to run deficits of around $1.2 billion/year, at least toward the latter part of the five year period, if not before.

This analysis also severely undermines the wisdom of the Governor’s proposed use of the state’s Statutory (and, if necessary) Constitutional Budget Reserves to “bridge over” the revenue reduction that will result from SB 21 for any period of time. The EconOne analysis demonstrates that, even if SB 21 results in a leveling off of production at current levels (0% decline), state revenues will never bounce back to current levels. Instead, again using the EconOne analysis at $100/bbl, even under the best case oil revenues likely will settle roughly at $5.1 billion — well below current levels.

The EconOne analysis demonstrates that to consistently reach $6.8 billion per year in revenues at 0% decline, average oil prices over the 30 year period would need to approach $120/bbl (in $2012). At a 1% decline rate, average oil prices over the 30 year period need to approach $130/bbl. Very, very, very, very few analysts predict those price levels.

As a consequence, using the state’s financial reserves to maintain current spending levels over even a short period is a “bridge” to nowhere. At the other end necessarily will be a precipitous drop in spending levels, much lower than if the the Budget Reserves had been maintained in the meantime as savings, with the earnings subsequently used as a supplemental source of revenue to soften the decline in oil revenues.

As I have explained previously on these pages, fiscal reform needs to go hand-in-hand with, if not precede, oil tax reform. The Governor is prioritizing the two in the exact reverse. The EconOne analysis demonstrates that following that approach walks the state straight out on a fiscal ledge, with nothing on the other side to grab hold of at the end.

Before the beginning of the current legislative session, the University of Alaska-Anchorage’s Institute of Social and Economic Research (ISER) advised the Legislature and others that “Alaska’s state government can afford to spend about $5.5 billion” in Fiscal Year 2014.

ISER also made the consequences of failing to follow that advice clear:

Right now, the state is on a path it can’t sustain. Growing spending and falling revenues are creating a widening fiscal gap. In its 10-year fiscal plan, the state Office of Management and Budget (OMB) projects that spending the cash reserves might fill this gap until 2023, as the adjacent figure shows.

But what happens after 2023? Reasonable assumptions about potential new revenue sources suggest we do not have enough cash in reserves to avoid a severe fiscal crunch soon after 2023, and with that fiscal crisis will come an economic crash.

Taking into account the late in session appropriations and following the Governor’s lead, the Legislature this year now appears to be on track to spend close to, if not beyond, $6.8 billion — $1.3 billion over ISER’s number. The consequences are clear. As ISER’s Dr. Scott Goldsmith explained during a hearing last week before House Finance, this session the Governor and Legislature effectively are passing the equivalent of a delayed tax hike on future generations.

Senator Pete Kelly, Co-Chair of Senate Finance said at one point this session, “[w]e have to slow this thing [overall spending] down …. It’s just ballooning, and we have to be the people who say, this far, and no farther on the budget.”

Ironically, at $6.8 billion, “this far” is the second largest regular session budget in Alaska’s history.

EconOne’s analysis, like ISER’s before it demonstrates that merely slowing down overall spending is not enough. Spending levels have to go in reverse, quickly, if Alaska is to avoid digging a deep hole for future generations.

Because the state necessarily will be drawing down the Statutory Budget Reserve in order to finance FY 2014 spending (in essence, engaging in deficit spending), next year’s “sustainable budget” level will be even lower than this year’s $5.5 billion. Sustainable budgets rely on retaining current reserves to help build the “nest egg” used to cushion future revenue levels. Like an individual’s retirement account, spending those reserves now, rather than investing them, lowers future earnings levels.

Continuing down the current road — as the Governor proposes in his 5-year Fiscal Plan — keeps digging the state’s fiscal hole deeper and deeper. What the EconOne analysis demonstrates is that we never come out the other side. Instead, even with oil tax reform and a production response that results in 0% decline, the state simply emerges at the end of the five year period at the edge of the fiscal cliff ISER describes in its study, perhaps even earlier than 2023.

During the interview about his Fiscal Plan, the Governor said that he intends to limit annual draws on the state’s reserves (i.e., deficits) to $700 million/year or less. But he also left at least two large loopholes in that commitment.

The first is that the limit “assum[es] the current forecast stays true.” We already know it won’t. The “current forecast” is based on ACES, which produces greater revenue over the short run than SB 21. The Administration has not yet prepared a forecast based on SB 21. As a result, with the passage of SB 21 the “current forecast” won’t remain true, near term revenues will be lower and the Governor will be positioned to justify increased draws because the forecast changed.

The second is the exception for “state-wide legacy projects.” Because those are additive to the budget, presumably they also are outside the limit on drawing down reserves.

More importantly, however, just as has occurred this session, the fact is once having set spending expectations at $6.8 billion, the Governor and Legislature likely will find themselves unable to restrict spending to lower levels, regardless of the draw on reserves. The difficulty of saying “no” to the current generation of recipients, once expectations are set, simply seems too difficult.

This session has been a disappointment in terms of fiscal policy. Exceeding sustainable spending levels by more than $1 billion shifts a substantial burden to future generations, and continues Alaska’s quick march toward the “economic crash” detailed in ISER’s report.

As I have explained elsewhere on these pages, the latter development also puts at substantial risk the very investment the state is trying to encourage through oil tax reform. In essence, the Governor and Legislature are undoing with one hand what they are trying to accomplish with the other.

The only greater disappointment than the results from this session would be if the Governor and Legislature continue down this road in subsequent legislatures, as outlined in the Governor’s 5-year Fiscal Plan. The EconOne analysis provides another data point showing that approach is a disaster.

Hopefully over the interim, both the Governor and legislators will realize that and chart another course. As a state, at least we should go into this with our eyes wide open.

One potential opportunity is through the House Subcommittee on Fiscal Policy created last week by Co-Chair Bill Stoltze in response to Rep. Charisse Millet’s HB 136. The Senate should create an opportunity to examine the issue as well.

Pingback: Recognition … | Thoughts on Alaska Oil & Gas