In an article responding to recent columns by Andrew Halcro and me, the Alaska Dispatch’s Amanda Coyne concludes that “Alaska’s oil tax myths, surprise, remain busted.” In reaching the conclusion, the Dispatch’s Coyne argues that “[b]y standards of the average guy — the one who isn’t getting rich working for the oil companies, the one who doesn’t have future political aspirations, and the one who, in fact, makes up nearly all of our majestic state — the oil-tax myths we busted remain busted.”

While I didn’t get the reference at first, a friend pointed out that the Dispatch’s Coyne apparently was attempting to be insulting at the same time as she was summing up her argument. Because I never have – and never will – run for office (heck, I couldn’t even get elected to the Board of the Alliance), I suppose I am the “one” she references who is “getting rich working for the oil companies.” Given the level of my contributions to, among others, the University of Alaska Anchorage, I am not sure my tax accountant would agree, but whatever.

Maybe the reason I didn’t get the reference, however, was because I was concentrating on the Dispatch’s larger mistake – that the “oil-tax myths … remain busted.” Here is the core of the Dispatch’s argument in support of their self-serving conclusion:

State Sen. Bert Stedman probably said it best during a committee hearing when he commented, “The average guy in the state… assumes that we’re taking 90 percent of every dollar. We don’t have a 90 percent tax rate.” … No we don’t, as us average folks understand tax rates to be. What the oil companies are focused on in Alaska is what’s called a “marginal” tax rate. That’s the tax rate on an additional dollar of income, rather than the total paid to the tax collector. That marginal rate has been used on both sides of the political aisle in the wider debate about taxation. For our purposes, however, let’s go back to the numbers, as we average folks see them. These numbers come directly from the Alaska Department of Revenue.

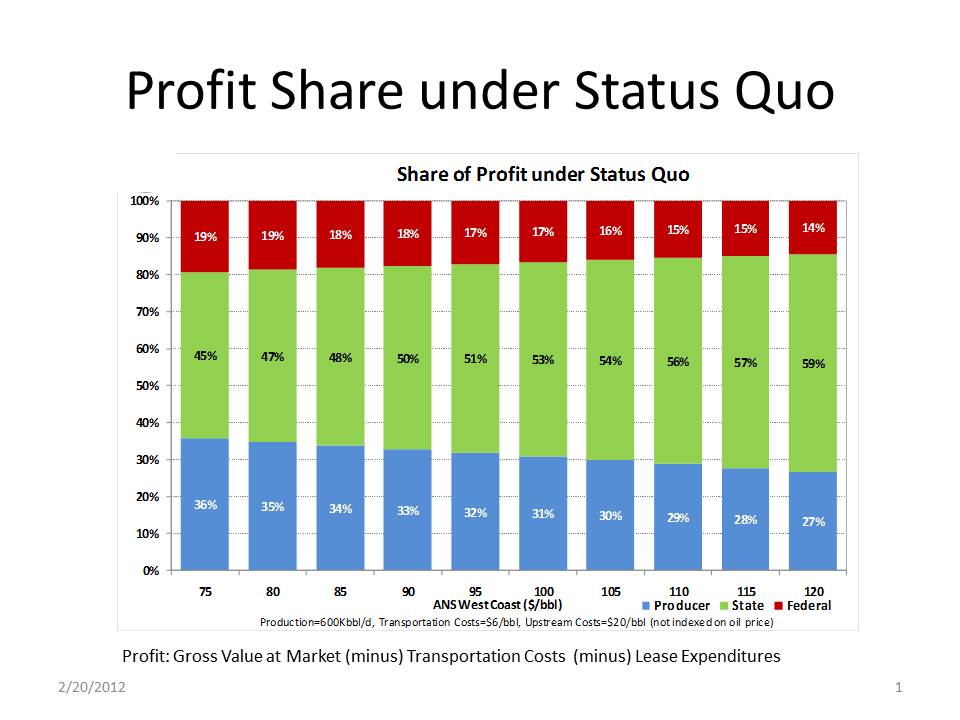

The Dispatch then returns to some numbers which incorporate, at $100/barrel oil, a state take rate of 53% and a federal take rate of 17%. While the Dispatch doesn’t make the calculation, that adds up to a combined take rate of 70%.

Actually, the Dispatch and I mostly agree on the state take number which, because of its structure, generally is within a few percentage points at both the weighted average and marginal level. For purposes of minimizing the number, the Dispatch prefers to state the number as roughly 40%, by converting the number to a percent of gross revenues, instead of stating it – as does the chart they reference and the remainder of the world – as a percent of profit. That approach creates a significant myth of the Dispatch’s own making, when the Dispatch then attempts to compare its contrived “40%” to other numbers calculated on a profits basis, from – to use their chosen universe – “Russia, Algeria, Angola, private lands in Texas and Louisiana, among many other oil taxing jurisdictions.” The result — combined with leaving out the federal tax effect in the calculation entirely — is falsely to create the impression that Alaska is a preferred economic alternative compared with other potential investment options.

But, semantics and false comparisons aside, the net dollar effect between the Dispatch’s approach to state take and mine is roughly the same.

Where the real differences surface is on what number to use for federal tax purposes. The Dispatch uses 17%; I use 35%, the federal marginal tax rate, in my commentary. Using 17%, the Dispatch’s numbers suggest that the real tax rate on industry is 70% at $100/barrel oil ($51.50 in combined taxes, divided by the $74 in profit derived from the chart). In my – and more importantly, investors’ – opinion, however, the real number that the Dispatch’s “average guy” should care about is 88%, the combination of the state take rate at 53% and the federal rate at 35%.

The differences begin as one of perspective. The 17% rate used by the Dispatch appears to be the weighted average federal tax rate paid by the industry over some period of time. Thus, the 17% rate is the number you would use if you viewed the purpose of the tax to operate as a type of windfall profits tax – to capture a percent of past profits that you believe is due government.

The 35% rate, however, is the rate that a company will likely pay on the revenues realized from new investments made to develop new production. Thus, it is the rate that investors use in projecting the effect of government take on potential future investments, and the number to use if you are assessing the competitive position of your state in attracting new investment versus alternative opportunities elsewhere in the world.

Why is that? Simple. The 17% results from the effect of the graduated approach to tax rates incorporated in the federal tax code, plus more significantly, various tax credits and adjustments arising out of investments made in the past both within and outside of Alaska. For example, the federal tax rate is 15% on the first $50,000 of income, 25% on the next $25,000 and so on until it flattens out at 35% above roughly $18 million. In addition, when Company A three years ago invested $100 million in a way that qualified for a federal tax credit, let’s say in North Dakota, the effective tax rate paid by the company was reduced below the 35% because of the effect of the credit. Both go to reduce the weighted average tax rate applicable in any given year. The result is a backward looking view at what the tax rate was at a given point in time for a company’s entire revenue stream.

Neither of these factors applies, however, when a company takes a forward looking view in projecting the economic effect of new investments, especially incremental investments in existing fields to develop new production – the type of investment that offers Alaska the biggest immediate opportunity to increase production levels. The reason is because most investors already have enough ongoing income to fill the existing graduated tax brackets. Thus, most investors correctly conclude that all of the additional income produced from the new investment will be taxed at the marginal, 35% rate.

In addition, especially if the incremental investment is being made in an existing field, the potential that the incremental investment will qualify for significant additional federal tax credits is small and, even if it does, the effect at best will likely last only a few years, while the production resulting from the investment likely will last several years into the future. Because the largest share of production will likely come after any credits expire, the total tax rate applicable over the life of the project likely will approach the 35% marginal rate, rather than anything significantly smaller.

Why does this matter to the “average guy”?

Again, the answer is simple. As I explained in my initial commentary in busting the Dispatch’s Myths No. 5 and 6, it matters because Alaska production is declining to levels significantly below those able to sustain Alaska’s current way of life both in the near and longer term. If the “average guy” is to avoid the consequences, that future needs to be reversed. In order to do that, new investment, substantial new investment – DNR Commissioner Dan Sullivan has estimated more than $4 Billion/year – is required to fund new development opportunities.

From that perspective, looking at the tax the same way that investors do is not only important to the “average guy,” it is critical.

The Dispatch pieces do not address this issue at all, dismissing the use of the marginal tax rate flippantly as “[w]hat the oil companies are focused on,” and thus, somehow, immediately suspect. The problem with that answer is that it is the oil companies that Alaska relies on for investment. As a consequence, what “they,” as potential investors, are focused on matters – and matters greatly – to the average Alaskan.

It is clear from the Dispatch’s explanation of the “average man” standard at the end of the most recent piece that it believes the purpose of the production tax is to act only as a means of extracting “Alaska’s fair share” of the value of production – in essence, to operate as a windfall profits tax. The Dispatch does not give any space to discussing its potential effect on development investment.

In my previous column, I explained that using the production tax to serve as a means for extracting Alaska’s “fair share” of oil revenues is an unjustified end run around the contractual commitments Alaska made at the time it first leased the acreage.

Even if you don’t accept that view, however, Alaskans concerned about more than this moment in time should focus on the effect that the state’s tax policy has on investment and, thus, both near and longer term production levels.

That is what the “average guy,” concerned about the value of his home, his standard of life and his kids’ education, should be doing, and why as a consequence he should be concerned about marginal tax rates. The Dispatch misleads itself and the “average guy” by suggesting he should not.

{kind=link}

Pingback: Busting the “Myth Busters”: Where the Alaska Dispatch Went Wrong | Thoughts on Alaska Oil & Gas

The Taxes are what they are and I, as an averge person, can see but one thing. I can see the large record breaking profits by the oil companies. So what does the taxes have to do with those profits. I can see the gas and diesel pump prices jump immediately when the barrel prices go up and a real slow almost non-existant drop in the price of gas and diesel when the price of the barrel falls. I don’t know about the other average person, but for the oil companies asking for tax breaks so they can make more profits off of me. Sounds like the oil companies wants us to bend over further than we already are and not bending over backward either.

LikeLike