Last Wednesday, Legislative Finance (LegFin) Director David Teal appeared before the Alaska House Finance Committee to discuss HB 115, the Committee leadership’s proposal to cut the PFD and institute income and capital gains taxes. The stated purpose of the presentation was to discuss modeling the impact of HB 115. As it turned out, however, the only impact of HB 115 that LegFin had considered was that on government revenues. The presentation didn’t even remotely touch on the impact of HB 115 on the overall Alaska economy — both the government and private sectors.

Last Wednesday, Legislative Finance (LegFin) Director David Teal appeared before the Alaska House Finance Committee to discuss HB 115, the Committee leadership’s proposal to cut the PFD and institute income and capital gains taxes. The stated purpose of the presentation was to discuss modeling the impact of HB 115. As it turned out, however, the only impact of HB 115 that LegFin had considered was that on government revenues. The presentation didn’t even remotely touch on the impact of HB 115 on the overall Alaska economy — both the government and private sectors.

Especially in the midst of a recession, we believe that effort — assessing the impact of HB 115 on the overall Alaska economy — is critical. Government fiscal policy plays a hugely influential role in the midst of a recession. It can make a recession better, but it also can make it worse, or even much worse.

Because, to our knowledge, none of the Administration, LegFin, the Chamber, or for that matter anyone else has undertaken the effort specifically to score the effect of HB 115 on the overall Alaska economy, we have decided to do so, using the factors developed last year in two studies done by economists at the University of Alaska-Anchorage’s Institute of Social and Economic Research (ISER). The first — Short-Run Economic Impacts of Alaska Fiscal Options — was published in March 2016 (the “March 2016 ISER Report”). The second — Permanent Fund Dividends and Poverty in Alaska — was published in October (the “October 2016 ISER Report”).

Taken together, and using the revenues projected to be produced by the various pieces of HB 115 in the presentation accompanying its first hearing before HFIN — State Revenue Restructuring Act HB 115 — we have assessed the impact on overall Alaska income, jobs, poverty and income disparity levels of the PFD cut and income tax portions of the bill. Because the ISER March 2016 Report did not consider the potential of a capital gains tax, we do not have the data to do an impact analysis of that portion of the bill. We would note, however, that the revenue expected to be raised by that portion of the bill — $85 million –is both a small part of the revenue to be raised through taxes ($655 million), and an even smaller part of the total amount to be raised through taxes and the use of Permanent Fund earnings ($2.25 billion).

As we will explain below, our analysis concludes that while in its best light the PFD cut and income tax portions of HB 115 may potentially save, on net, about 4,000 government and government-related jobs, that will come at the expense of lowering overall state income, increasing the income disparity between low and high income Alaskans and, of huge concern, likely pushing at least an additional 8,500 or so — more than double the number of jobs being saved — and possibly even more Alaskans, below the poverty line.

In other words, saving those 4,000 net jobs will be financed on the backs of reduced overall Alaska income, a staggering increase in Alaska poverty and significantly increased income disparity.

This is how we arrive at those conclusions.

Income and Jobs

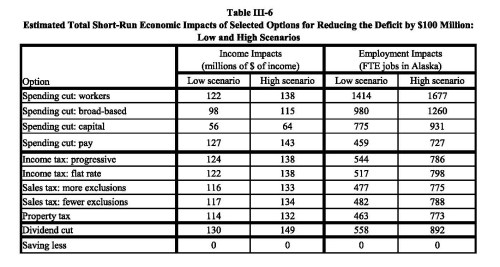

As we have discussed previously on these pages (“Why we believe cutting the PFD has the largest adverse impact on the overall Alaska economy,” Jan. 21, 2017), the March 2016 ISER Report contains a chart that enables a reader easily to estimate the impact on jobs and income of various fiscal options. For ease of reference, we repeat it here:

The chart estimates the impact of the various fiscal options it addresses per $100 million of deficit reduction. So, for example, cutting the PFD by $100 million would reduce overall Alaska income by between $130 – $149 million, and result in the loss of 558 – 892 jobs.

An important thing to recall in any analysis is that, usually, each step has offsets. So, for example, if the government used the money “saved” by cutting the PFD by $100 million instead to fund $100 million in capital spending, overall Alaska income would be reduced by between $130 – $149 million as a result of the PFD cut, but increased by $56 – 64 million as a result of the capital spending, with a net negative effect on overall Alaska income of between $74 – 85 million. The related jobs calculation would show a net positive of between, but only between 39 – 217.

Another important thing to recall is that, on the government spending side, new revenue won’t be focused just on maintaining employment (i.e., avoiding “Spending cut: workers”), a capital budget (i.e., avoiding “Spending cut: capital”) or pay scales (i.e., avoiding “Spending cut: pay”). Instead, new revenue will likely be spread across all three sectors, which is captured elegantly by the category “Spending cut: broad-based”.

Estimating the adverse impact of the PFD cut contained in HB 115 on the overall Alaksa economy requires addressing another issue. At one level, estimating the proposed extent of the PFD cut is simple. The analysis could calculate it simply as the difference between the level of the PFD disbursement estimated by the Permanent Fund Corporation for FY 2018 (currently estimated to be $1.539 billion, see ALASKA PERMANENT FUND FUND FINANCIAL HISTORY & PROJECTIONS as of November 30, 2016) and the PFD level estimated for the same year in the HB 115 analysis ($762 million).

But on this page we generally have taken the position that in the course of implementing Hammond 50/50 (i.e., the use of one half of the Permanent Fund earnings stream each for dividends and “essential government services”) the amount of money taken annually from the Permanent Fund earnings stream should be fixed at a specified percent. Consistent with that approach, the amount of the PFD cut proposed under HB 115 would be somewhat smaller, equal to the difference between the amount of the PFD as it would exist under Hammond 50/50 at the specified percent and the amount proposed under HB 115.

To reflect that, in our analysis we have calculated the impact of the PFD cut contained in HB 115 two ways: first, by using the PFD level estimated by the Permanent Fund Corporation in their most recent Financial History and Projection ($1.54 billion), and second, to keep it simple by using the PFD level which would result from using Hammond 50/50 at the 4.75% rate used in HB 115. Using the data included in last week’s presentation on HB 115, that implies a total draw rate of around $2.25 billion and a PFD of around $1.13 billion.

Applying these factors to HB 115 produces the following results on overall Alaska income and jobs. (For simplicity’s sake, the following analysis uses the midpoint between the “low” and “high” scenarios contained in the ISER chart above rather than inject yet more numbers into what already is a numbers-laden analysis.)

To summarize, comparing HB 115 to a continuation of the current approach to the PFD, the PFD cut and income tax portions of the bill reduce overall Alaska income by roughly $840 million annually and result in saving roughly a net 1,000 jobs. Comparing HB 115 to the adoption of the Hammond 50/50 approach using a fixed draw rate of 4.75%, the PFD cut and income tax portions of the bill reduce overall Alaska income by roughly $270 million and result in saving roughly a net 4,000 jobs.

But that is only part of the story. To understand the full story, it is important also to understand the effect of the PFD cut and income tax portions of HB 115 on income disparity and poverty levels.

Poverty and Income Disparity

As we also discussed in our January 21 piece on these issues, the October 2016 ISER Report contains an analysis of the effect on Alaska poverty levels of cutting the PFD, and the March 2016 ISER Report contains an analysis of the effect on various Alaska income segments of both cutting the PFD and implementing an income tax.

The effect of cutting the PFD on poverty levels is summed up on this slide from the October 2016 ISER Report:

The effect on income disparity is addressed in Section II of the March 2016 ISER Report. The approach and analysis used in the Report to estimate the effect of PFD cuts and income taxes on the ends of the Alaska income spectrum can be summed up as follows:

To analyze how different taxes and a dividend cut might affect Alaskans at different income levels, we divided Alaska households into ten groups, based on their per-capita incomes. … Each group represents about 29,000 households …. Income reported in the 2014 census data [the latest available at the time the report was prepared] represents income earned in 2013. Households in the richest ten percent earned on average more than $200,000 that year, while those in the poorest ten percent earned less than $14,000 …. The top ten percent of households accounted for 21 percent of all personal income—only a little less than the bottom 50 percent of households combined ….

…

Reducing Permanent Fund dividends would cost the poorest households the most, in both dollars and in percentage of income. Reducing the PFD by $156 per person and diverting the revenue to state government would raise $100 million. But only the poorest households would actually lose the full amount. Most households would get a portion of the lost income back in reduced federal income taxes, but the poorest households might not have any income tax liability. The higher the household’s per capita income, the more the federal taxes would be reduced and the PFD loss offset. Per-person disposable income of the richest ten percent of households would fall on average $112.

The dollar losses for the poorest households [per $100 million cut] amount to 3.3 percent of their per-person disposable income—compared with 0.1 percent for the wealthiest households. …

…

The income tax options would cost the wealthiest households 70 to 160 times as much in dollars as the poorest, which have very little income to tax. These are the only options that would cost the wealthiest households a higher percentage of their incomes. … The 10 percent income tax surcharge is more progressive, following the progressive structure of the federal income tax. Even with the progressive rates, the income tax surcharge would reduce per-capita disposable income of the richest ten percent of households by about 0.5 percent per $100 million raised. …

Using the same approach as taken in the previous section, applying these factors to the PFD cut and income tax portions of HB 115 produces the following results of the effect of the bill on Alaska poverty and income disparity levels.

To summarize, comparing HB 115 to a continuation of the current approach to the PFD, the PFD cut portion of the bill would increase the number of Alaskans below the poverty line by roughly 15,600 and result in increasing income disparity between the highest and lowest income Alaskans by reducing the disposable income of the lowest 10% of households by income by over 25%, but only reducing the income of the highest 10% by 5%.

Comparing HB 115 to the adoption of the Hammond 50/50 approach using a fixed draw rate of 4.75%, the PFD cut and income tax portions of the bill would increase those Alaskans below the poverty line by roughly 8,500 and result in increasing income disparity between the highest and lowest income Alaskans by reducing the disposable income of the lowest 10% of households by income by over 12%, but only reducing the income of the highest 10% by roughly 4.5%.

Some supporters of HB 115 have argued that the income tax portion of the bill would help to balance out the income disparity effects of the PFD cut. The above analysis indicates that while the income tax provisions lessen the disparity effects which would result from adopting a PFD cut alone, the bill still significantly widens the income disparity between high, middle and low income Alaskans by imposing a significantly greater burden for financing government (as a percent of income) on lower income Alaskans than on higher income Alaskans. As demonstrated in the previous section, this, in turn, also contributes to an absolute reduction in overall Alaska income levels.

Conclusion

From the perspective of the overall Alaska economy, the PFD cut and income tax portions of HB 115 — the portions we are able to analyze utilizing the tools provide by the March and October 2016 ISER Reports — represent bad fiscal policy, especially during a recessionary period.

Recessions generally occur when there is a widespread drop in spending. While the PFD cut and income tax portions result in saving, on net, some government and government-related jobs and may also benefit some government-related businesses, they nonetheless result in further reductions in overall Alaska income, which is a more direct measure of spending in the economy than raw jobs (which apparently do not result in generating as much income in the Alaska economy as keeping the money in the hands of those receiving the PFD).

As importantly, however, the PFD cut and income tax portions of HB 115 also result in a significant increase in Alaska poverty and income disparity levels. This means that the gains being claimed by supporters to result from the PFD cut and income tax portions of HB 115 — a net plus in jobs — is being financed largely on the backs of lower and middle income Alaskans. Doing that at any time is questionable; doing it when that same segment of the population is suffering through a recession is something beyond that.

If they truly are concerned — as we believe they should be — about the effect of the proposed legislation on the overall Alaska economy and Alaska poverty and income disparity levels, the supporters of HB 115 should return to the drafting table and make significant revisions designed to remake the bill into additive — rather than negative — fiscal policy.

In any event, going forward any fiscal bill being considered by the Governor or Alaska legislature should be analyzed and scored for its effect on the overall Alaska economy. As demonstrated above, running blind can lead to bad results.

___________________________________

This post first appeared on Alaskans for Sustainable Budgets, a new blog focused on News & Commentary on Alaska oil, gas & fiscal policy on national website Medium.

I used to be opposed to fiscal certainty, not any more. Although, I never did like the idea of gouging just to gouge the oil companies.

I paid state income taxes before they were dropped in the 80s.

The idea of capital gains . . . that is a typical liberal attack on the accumulation of wealth.

Bill Walker comes up for reelection next year.

I hope the Rs can get their act together.

Somebody needs to.

LikeLiked by 1 person

Pingback: Comparing the impact of SB 70 v. HB 115 on the overall Alaska economy … | Thoughts on Alaska Oil & Gas