Recently, I wrote a piece entitled “Alaska Fiscal Policy| Where We Have Gone Wrong.” In it, I analyze state spending levels since the beginning of the Palin/Parnell Administrations, compare that to what is sustainable given the state’s financial and natural resources and conclude that “Alaska’s most recent generation of political leaders … is leading Alaska off the fiscal cliff.”

This is the closing paragraph: “It is ironic that a Legislature and Administration that claim to be ‘fiscal conservatives’ have painted the state into this fiscal corner — but the fact is that is exactly what they have done in the last six years. Going forward, reverting to truly ‘sustainable’ spending levels is essential if Alaska is going to return to the right track.”

Some readers responded to the piece by asking what can be done to bring state spending within sustainable levels. This piece is part of the answer.

Background – Addressing the Federal Fiscal Problem

Most of the readers of these pages will be familiar with Grover Norquist, Americans for Tax Reform (“ATR”) and the “Taxpayer Protection Pledge.” The words of the Pledge are slightly different at different levels of government, but the basics are simple. The signer pledges that he or she “will oppose and vote against any and all efforts to increase taxes.”

At its core, ATR and its affiliate, the Center for Fiscal Responsibility (now, the Cost of Government Center), are concerned about the financial burden that current government actions are imposing on future generations of Americans. They believe excessive current federal government spending levels are leaving future generations with a staggering debt, which will necessitate continued high tax rates.

The ATR’s Taxpayer Protection Pledge is an effort to restrain taxes, in order to restrain current spending and improve the situation otherwise to be faced by future generations. In the absence of bringing current spending under control, some – including the Congressional Budget Office – estimate that, for the first time, future generations of Americans will have a lower standing of living than previous generations.

Alaska imposes no significant taxes at the state level, other than on the oil industry, and consequently the Taxpayer Protection Pledge has never gained much traction in Alaska with regard to state government and tax policy. However, the looming fiscal crisis facing Alaska which is outlined in the earlier piece is of comparable gravity to the federal problems driving Norquist’s Taxpayer Protection Pledge and imperils future generations of Alaskans in much the same way.

Alaska Faces a Comparable Fiscal Crisis

Alaska faces a comparable and equally dire fiscal crisis to that which has developed at the federal level. Due to current excessive state government spending, future Alaskans – which will include many of the current generation as they enter retirement – are facing a lower standard of living than present day Alaskans. As a consequence, Alaska needs its own state level statute restricting excessive spending and may benefit from a pledge to support it.

Alaska’s situation is created by somewhat different factors than at the national level, but the effect is the same. At the current rate of state spending, future Alaskans will be faced either with paying significant tax rates in order to support the same level of government goods and services enjoyed by the current generation, or suffer significant reductions in government services and support because of lack of funding.

The reason is that at some point – and that point may be as early as next year if Alaska North Slope oil drops to $90/barrel – state spending levels will start outstriping revenue levels, even at current oil tax rates. Given the anticipated continued steep decline in current oil production rates, once the line is crossed into deficit spending it is unlikely that Alaska ever will return to the black as long as current spending rates continue.

Two existing savings accounts – the Statutory Budget Reserve and the Constitutional Budget Reserve – will cushion the effect of deficits for a time, perhaps as long as several years. During that time, spending levels – and the current standard of living –will be artificially sustained by drawing down the Budget Reserves. Once the Reserves are exhausted, however, a huge and growing deficit will exist between state spending and state revenue levels.

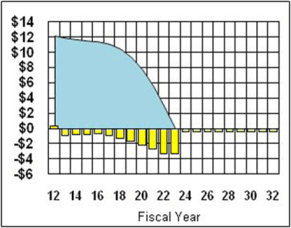

Two charts from “Revising the State Fiscal Plan to Account for Petroleum Wealth,” a study published last year by the University of Alaska Anchorage’s Institute for Social and Economic Research (“ISER”), make the point graphically.

The first chart, which is based on the scenario outlined on page 5 of the study (“OMB FISCAL PLAN—EXTENDED (2012 Billion $), NO GASLINE, 75% OF DOR OIL REVENUES”), shows state spending levels as a black line, oil revenues in green and withdrawals from the Statutory and Constitutional Budget Reserves in yellow. The numbers on the left are billions of dollars; the numbers across the bottom are fiscal years. At the assumptions made in the chart – which roughly duplicate the most recent forecasts made by the State of Alaska Office of Management and Budget (“OMB”) at $90/barrel oil – Alaska state government starts experiencing budget deficits (i.e., current spending exceeds current revenue) next year, in Fiscal Year 2013. The chart assumes that withdrawals from the two Budget Reserves are used to plug the gap for as long as the Budget Reserves last.

The first chart, which is based on the scenario outlined on page 5 of the study (“OMB FISCAL PLAN—EXTENDED (2012 Billion $), NO GASLINE, 75% OF DOR OIL REVENUES”), shows state spending levels as a black line, oil revenues in green and withdrawals from the Statutory and Constitutional Budget Reserves in yellow. The numbers on the left are billions of dollars; the numbers across the bottom are fiscal years. At the assumptions made in the chart – which roughly duplicate the most recent forecasts made by the State of Alaska Office of Management and Budget (“OMB”) at $90/barrel oil – Alaska state government starts experiencing budget deficits (i.e., current spending exceeds current revenue) next year, in Fiscal Year 2013. The chart assumes that withdrawals from the two Budget Reserves are used to plug the gap for as long as the Budget Reserves last.

The second chart shows the combined size of the two Budget Reserves and the effect of the withdrawals that will be necessary to maintain the projected level of spending. The size of the Budget Reserves at any given point in time is shown in blue; the level of annual additions (FY 2012 only) and withdrawals (FY 2013 – FY 2013) are shown in yellow. This scenario assumes the continuation of the spending levels included in the first chart.

The combined effect of the two charts is to demonstrate that by FY 2023, both Budget Reserves are exhausted and there is no remaining source of funds – short of starting to draw down the Permanent Fund — available to cover the shortfall between state spending and revenue levels. The more recent OMB forecasts now show reaching that point two years earlier, in FY 2021.

Regardless of whether the point at which the Budget Reserves are exhausted comes in 2023 (as projected in the ISER study), 2021 (as most recently projected by OMB) , or at some other time, at that point the state will be faced with three options:

- start tapping the Permanent Fund to cushion the effect of excessive spending for an additional number of years (at the expense of reducing, then terminating the Permanent Fund Dividend);

- establish other sources of revenue, such as a state sales or income tax; or

- implement drastic cuts in state spending and government programs.

Any of the three, however, will ensure that those in Alaska at that time will endure a lower standard of living than those who have come before.

The Future Doesn’t Have to be This Way

The future doesn’t have to be this way. In another recent study (“Managing Alaska’s Petroleum Nest Egg for Maximum Sustainable Yield“), ISER demonstrates that if Alaska state government restrains current spending to a “sustainable” level, the future stream of earnings from the savings that have been accumulated to this point and are generated going forward can support continued spending at the same level (adjusted for inflation) virtually in perpetuity.

The ISER approach operates in much the same way as an individual’s retirement account. At some point, all of us know that our earning power will go down, or end, as we enter retirement. To prepare for that day we put into savings now an amount of money which, through investments and additional savings, we anticipate will grow to a certain amount by the time we retire. That amount, in turn, will then produce a certain amount of revenue going forward on which we will live in retirement.

We know that the more we put into savings, the more income we have in retirement. Conversely, we know that if we choose to spend the money now rather than save it, we will have less income in retirement. Financial analysts help us calculate the amount we need to save now in order to hit a target level of income in retirement.

The ISER analysis approaches state government spending in the same way, treating the state’s decline in oil revenue the same as gradually phasing into retirement. Taking into account current savings and the anticipated future – but steadily declining – revenue stream from oil, the ISER study calculates the amount of spending – and savings – state government needs to engage in now, in order to ensure that future Alaskans continue to enjoy the same level of goods and services as current Alaskans, even as oil production and the associated revenues decline.

The ISER study calls the resulting spending level – that which needs to be implemented now in order to maintain the same level on into the future – the “maximum sustainable yield.” That terminology is derived from Article VIII, Section 4 of the Alaska Constitution, which provides that “Fish, forests, wildlife, grasslands, and all other replenishable resources belonging to the State shall be utilized, developed, and maintained on the sustained yield principle, subject to preferences among beneficial uses.”

ISER’s point is that, just as the state limits the take of fish each year in order to ensure that there are relatively the same amount of fish also in the future, the state needs similarly to limit its level of fiscal spending each year in order to ensure that there also is relatively the same amount of government income to spend into the future.

At currently projected spending, oil price and production rates – the three key factors in the calculation – the “maximum sustainable yield,” in other words, the maximum sustainable spending rate from the General Fund, is $5.35 billion per year. This compares with government spending from the General Fund during the current Fiscal Year of $6.8 billion and projected spending under next fiscal year’s budget – passed by the Legislature and signed by the Governor – of an all time record $7.6 billion.

There may be some room for quibbling at the margins about ISER’s methodology and calculations. Perhaps the current “maximum sustainable level” is $5.75 billion, or possibly just $4.9 billion. Future commentaries here and elsewhere will no doubt explore what should be the precise approach to the calculation. But those quibbles are just that. Having spent a great deal of time with ISER’s analysis, I am confident that directionally ISER has developed a comprehensive and robust approach to calculating what is Alaska’s “sustainable” government spending level. Capturing that in words – to put into statutory language – will not be difficult.

Which brings us back to the reason for this piece – to articulate “what can be done” to return Alaska to truly sustainable government spending levels and thereby avoid sentencing future generations of Alaskans necessarily to a lower standard of living.

The Statute

My thought is this. At the beginning of the next legislative session, Alaska’s Governor should propose, and the Alaska Legislature should enact, a statute which limits the annual budgets that the Governor can propose, and the Legislature can enact, to an amount no greater than the “maximum sustainable” spending levels calculated using the ISER approach.

The Director of the Office of Management and Budget – the person responsible for developing and explaining the Governor’s proposed budget – would be directed to calculate and announce the maximum sustainable spending level by October 1 of each year. This figure would function as a spending ceiling and the Governor would be limited to that amount in proposing his budget for the coming year.

The Legislature could reorder priorities within the amount or provide for increases up to that amount if the Governor’s initial budget fell below the ceiling, but would be prohibited from enacting a final budget in excess of the amount. As a safeguard, the Governor would be directed to exercise his line item veto authority to reduce the budget passed by the Legislature back to the sustainable level should the Legislature not comply. As an additional safeguard, the Alaska Supreme Court would be vested with the authority to enforce the statute should both the Legislature and Governor fail in their responsibilities.

There would be only two exceptions to the rule.

First, to deal with true emergencies, the cap could be overridden in a given year by a vote of 80% in each legislative body and agreement of the Governor. This hurdle should be sufficient to prevent the Legislature from circumventing the ceiling in order to finance continued ordinary spending, but not too high to prevent action in the event of a true emergency.

Second, the Governor could propose, or the Legislature could enact, additional spending above the “sustainable” limits, but only if the body doing so also proposed, and all three bodies subsequently enacted, additional sources of “sustainable” revenue above those resulting from the ISER calculation. In short, if a Legislature wanted to spend additional money above sustainable levels, it would have to establish an additional source of revenue – it couldn’t simply raid the amounts being set aside for future Alaskans.

So, for example, if future legislators want to propose, as has the most recent Legislature, spending state funds to put Astroturf on middle school playgrounds, or to rebuild at state expense a parking lot at a privately owned sports facility, or to pay for 1500 plane tickets so that some people from outside Anchorage can spend their Thanksgiving vacation in town, then, fine, propose a source of additional, sustainable revenues, such as a statewide sales or income tax, to fund those expenditures. But the Legislature would be restricted from raiding the financial reserves set aside to support future Alaskans in order engage in those activities.

The Pledge

But how to assure that legislative candidates in the upcoming election, who might otherwise give lip service to the proposal, become genuinely committed to the principle, so that voters supporting the proposal reasonably can judge whether their representatives will act consistent with their wishes on the issue?

“Forgetfulness” has been a continuing problem at the federal level. Candidates might talk tough about the federal debt during a campaign, but change course when faced with pressure after the election from various interest groups who benefit from continued government spending. Given the level of state government spending today – and the number of interest groups that have become dependent on it – the same challenge exists in Alaska.

This is where the title of this piece and the opening reference to Grover Norquist’s taxpayer pledge come in handy.

A thought is to provide all legislative candidates this coming election with the opportunity to sign a simple pledge, similar to that used by Americans for Tax Reform, which would read as follows:

“I, ____________, pledge to the voters of (Senate or House) District __, and to all the people of this state of Alaska, that I will vote in favor of legislation to cap state spending at the maximum sustainable spending level, and thereafter will propose and only vote for state operating and capital budgets which implement that cap.”

The list of candidates signing the Pledge, and those not by two weeks before each election, could then be listed on a website maintained by a state group, similar to Americans for Tax Reform. This state level group could undertake the responsibility for monitoring the progress of the pledge and subsequent implementation of the statute. A working title for the group could be Alaskans for Fiscal Sustainability.

Publicizing those signing the Pledge, and those not, would enable voters to judge for themselves which candidates are committed to Alaska’s future, and which are not. In competitive legislative races in most districts, we can envision that those signing the Pledge could gain a distinct advantage over those who have not.

Not surprisingly, even with a limited rollout of the idea which followed the first piece on this subject, several current legislators and candidates, both R’s and D’s, have expressed interest in signing the Pledge.

Your Thoughts

We would welcome your thoughts on the idea as it gestates; we encourage you to send them to Alaskans4FiscalSustainability@gmail.com.

Thank you! It’s good to see there is recognition of the dismal state of Alaska’s economy and the silent alarm surrounding the massive operating and capital budgets! (Although who doesn’t favor more infrastructure!)

LikeLike

Pingback: “Understanding Alaska’s Budget” May Explain Much More Than It Intends … | Thoughts on Alaska Oil & Gas

Pingback: The most important slide in this election … and why I have contributed to Mike Dunleavy and Jeff Landfield | Thoughts on Alaska Oil & Gas

Pingback: Alaska Budget Cutting: Its Not Rocket Science … | Thoughts on Alaska Oil & Gas

Pingback: Don Smith for Senate H … | Thoughts on Alaska Oil & Gas